According to media reports, Apple and Intel have reached a preliminary chip-manufacturing agreement, under which Intel may produce certain chips for Apple devices in the future.

The news sent Intel shares soaring 15%; Source: CNBC.

On the surface, this may look like a rekindling of an old relationship: Apple once used Intel processors in Macs, later replaced Intel with Apple Silicon, and now may hand part of its chip-manufacturing orders back to Intel. That narrative is dramatic enough, but it also makes it easy to misread the real meaning of this development.

01 Apple Is Not Returning to the Intel CPU Era

Over the past forty years, every major choice Apple has made in chips has, in essence, not been a simple supplier switch, but a reallocation of product-definition power.

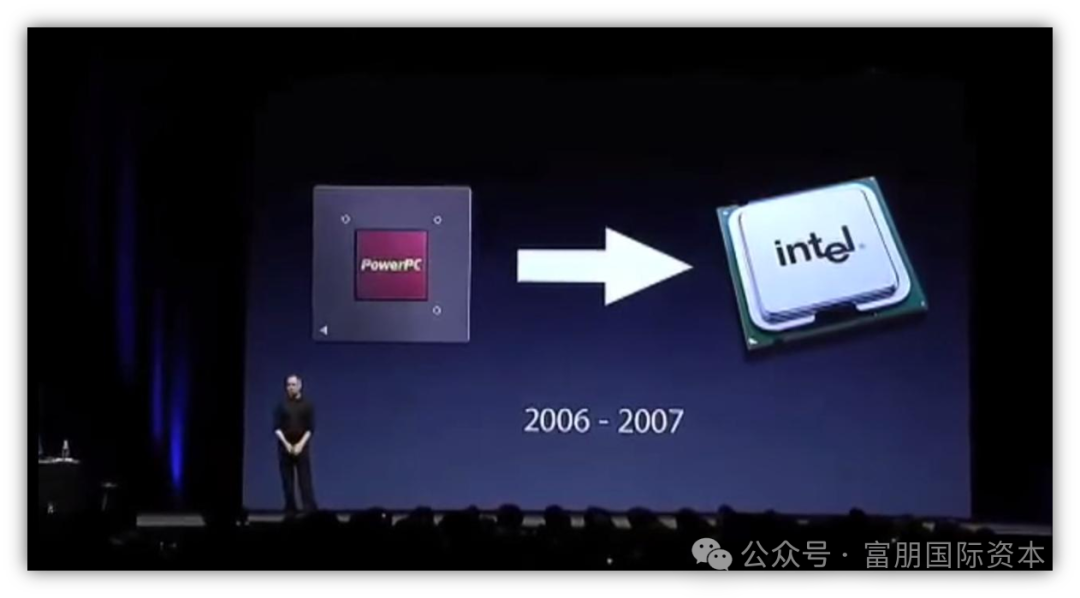

Early Macintosh computers used Motorola’s 68000-series processors. In the 1990s, Apple shifted to the PowerPC architecture jointly advanced by Apple, IBM, and Motorola, hoping to differentiate itself from the traditional PC camp. In 2005, Steve Jobs announced at WWDC that the Mac would move from PowerPC to Intel processors, and the first Intel Macs launched in 2006. The core reason for that transition was not that Apple suddenly preferred Intel, but that PowerPC had encountered bottlenecks in performance-per-watt and mobile adaptation in the notebook era, while Intel at the time had stronger process capabilities, performance roadmaps, and mass-production certainty.

In 2005, Steve Jobs announced at WWDC that the Mac would use Intel chips; Source: iMore.

But history did not stop in the Intel era.

With the rise of the iPhone and iPad, Apple gradually realized that what truly determines the end-user experience is not only the operating system and industrial design, but also the underlying chip. In 2008, Apple acquired the low-power chip design company PA Semi, laying the groundwork for its later in-house A-series chips. After that, Apple continuously refined the A-series processors on the mobile side and gradually built its own chip-design capability.

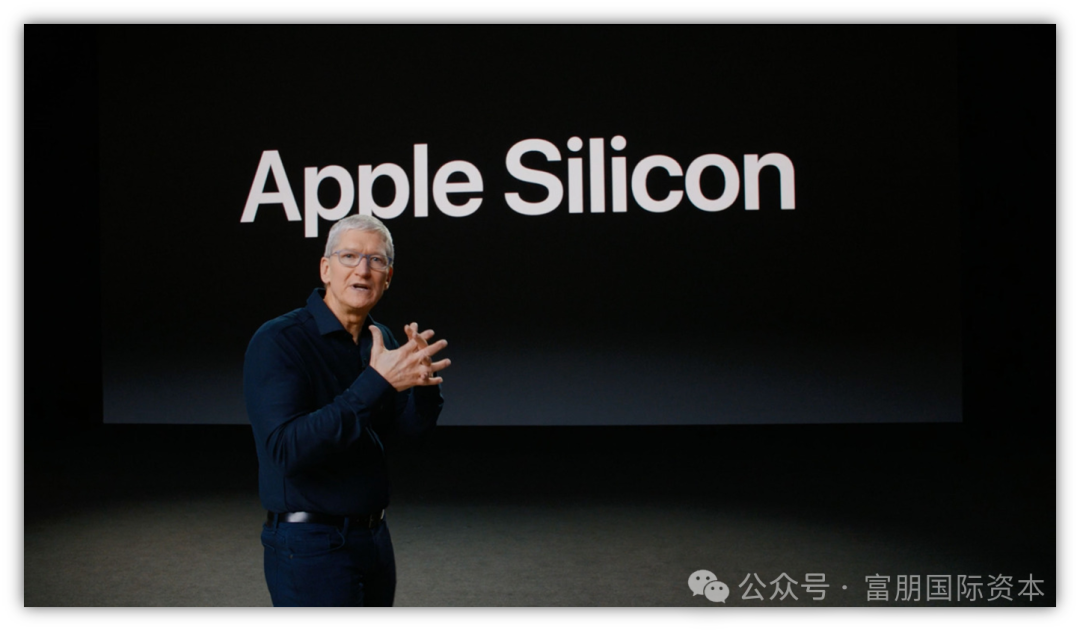

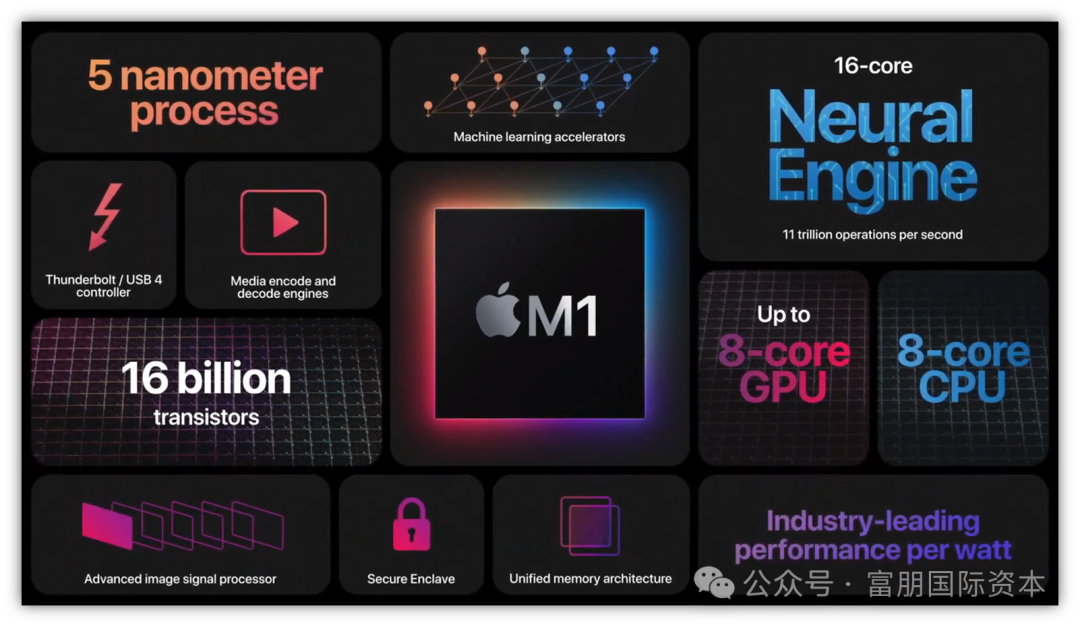

This path ultimately led to a historic leap in 2020: Apple officially announced that the Mac would transition from Intel processors to Apple Silicon. The launch of the first-generation M1 chip marked the point at which Apple was no longer simply buying general-purpose CPUs, but began redefining the Mac through its own system-on-a-chip (SoC).

Apple Silicon is not merely an “Apple-branded CPU,” but a highly integrated system-on-a-chip platform that includes the CPU (Central Processing Unit), GPU (Graphics Processing Unit), Neural Engine, video encode/decode modules, security modules, and a unified memory architecture. For the first time, it allowed Apple to place chips, systems, software, and end-user experience on the same roadmap.

In 2020, Tim Cook unveiled Apple Silicon, bringing years of Apple’s technological accumulation into the spotlight and commercializing it; Source: AppleInsider.

So, the most accurate summary of Apple’s chip strategy over the past decade is not “de-Intelization,” but rather this: Apple moved from buying chips defined by others to defining its own chips; from adapting to the pace of suppliers to controlling the pace of its own products. But it is important to note that what Apple has achieved is autonomy over chip design, not autonomy over chip manufacturing.

From the A-series to the M-series, Apple is responsible for design, but it is TSMC that actually manufactures these advanced chips. In other words, the success of Apple Silicon has been built on the combination of “Apple design + TSMC manufacturing.” Relying on advanced process technology, yield control, production stability, and advanced packaging capabilities, TSMC has become the most important manufacturing partner in Apple’s in-house chip era.

That is precisely why the possibility of renewed cooperation between Apple and Intel appears especially nuanced today. If Intel manufactures chips for Apple in the future, the logic will not be “Intel designs the CPU and Apple buys and uses it,” but rather:

Apple continues to design Apple Silicon, while Intel participates as a foundry in part of the manufacturing.

This means the core of the Apple–Intel relationship has changed.

In 2006, Apple chose Intel in order to escape the performance-per-watt constraints of PowerPC.

In 2020, Apple abandoned Intel in order to escape the limitations that Intel’s general-purpose CPU roadmap imposed on the Mac’s cadence.

And today, Apple is re-engaging with Intel not to return to the past, but to find, in the AI era, a second advanced-process option for Apple Silicon beyond TSMC.

For the first time, Apple has truly begun to look for an advanced-process option beyond TSMC for the Apple Silicon ecosystem.

02 Why Apple Was Willing to Keep Almost All Its Eggs in TSMC’s Basket in the Past

From a basic business perspective, Apple has never liked relying on a single supplier.

It lets BOE, Samsung, and LG compete for display orders; it lets Foxconn, Pegatron, and Luxshare share assembly capacity; and it maintains multiple supply sources for key components. Yet when it comes to advanced chip manufacturing, Apple has long been highly dependent on TSMC.

The reason is simple: advanced process technology is not ordinary manufacturing—this is not something just anyone can do. Apple chose TSMC because TSMC built almost irreplaceable advantages in three areas.

1. TSMC’s advanced-process stability is stronger

Chip manufacturing is not just about the name of the process node. It is not the case that if you also call it 3nm or 2nm, you can necessarily supply Apple. What truly determines whether Apple dares to place an order is:

- yield

- power efficiency

- mass-production stability

- defect rate

- delivery cadence

- collaborative capability with Apple’s design teams

Apple’s product cycle is extremely rigid. The iPhone launches every year, and the Mac and iPad each follow their own cadence. For Apple, chip supply cannot merely “work in the lab”; it must be manufactured stably across products in the tens or even hundreds of millions of units. That has been TSMC’s greatest strength: it can not only make advanced processes, but can also reliably turn them into commercial production capacity.

2. TSMC’s advanced packaging capability has become increasingly critical

In the past, when people talked about chips, they mainly talked about process nodes. But in the AI era, advanced packaging has become just as important.

Packaging technologies such as CoWoS, SoIC, and 3D IC have become key bottlenecks for AI chips and high-performance computing chips. Nvidia’s Blackwell and other AI chips are highly dependent on TSMC’s advanced packaging capabilities, and TSMC is also expanding CoWoS and 3D-IC capacity in Arizona, with plans to establish those capabilities before 2029.

This illustrates one point: TSMC’s real moat is no longer just wafer manufacturing, but a systems capability combining “advanced process + advanced packaging + large-scale mass production.”

Apple’s past bet on TSMC did not mean it failed to understand that “you shouldn’t put all your eggs in one basket.” It was because, in the realm of the most advanced chip manufacturing, there was, for a long time, effectively only one qualified basket—and that was TSMC.

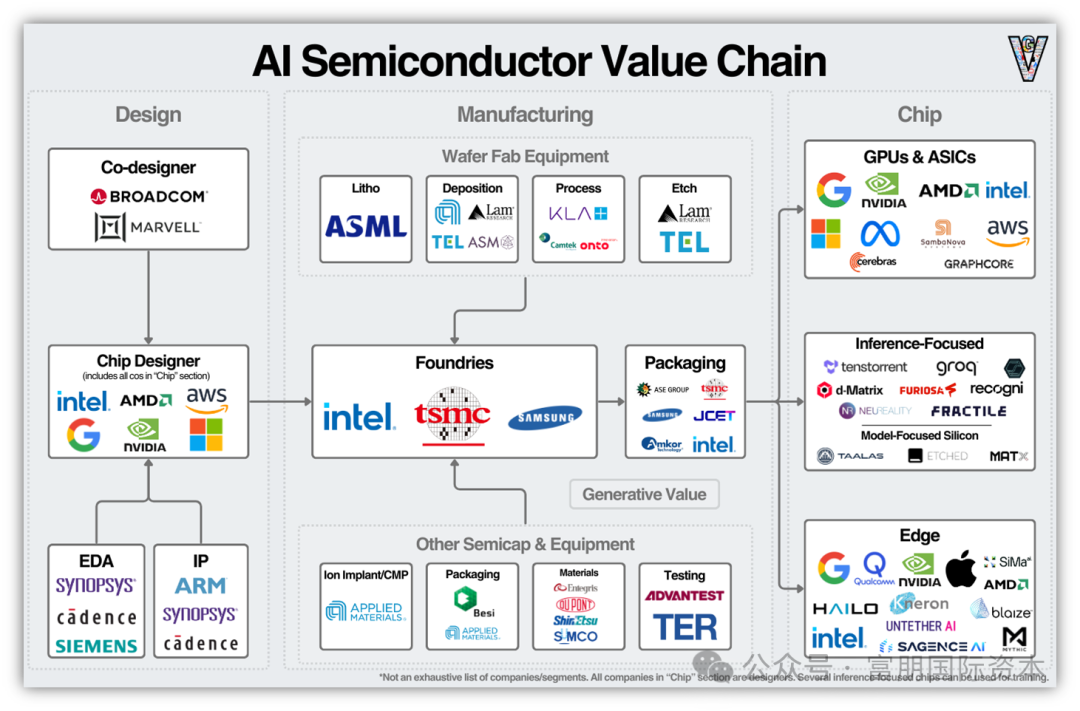

Overview of the AI semiconductor value chain, in which TSMC occupies a critical position; Source: Eric Flaningam.

3. Intel was not an ideal foundry choice for Apple in the past

Many people ask: isn’t Intel a chip giant? Why didn’t Apple have Intel manufacture for it earlier?

That is precisely the heart of the issue. Intel was once powerful because it controlled both chip design and chip manufacturing at the same time—the so-called IDM model. It designed its own CPUs, manufactured its own CPUs, and dominated the PC era under the banner of “Intel Inside.”

But that model also planted hidden risks.

In the PC era, Intel’s manufacturing system primarily served its own products, rather than serving large numbers of external customers the way TSMC did. TSMC operates as a pure-play foundry, with customers including Apple, Nvidia, AMD, and Qualcomm. Its organizational capabilities, IP ecosystem, customer-collaboration processes, confidentiality mechanisms, and process-adaptation capabilities were all built around serving external customers.

Intel’s problem in the past was that it was very good at making chips for itself, but not necessarily very good at making chips for others. That is why Intel’s effort to become a foundry has never been easy. Foundry is not just about opening up production lines; it requires the establishment of an entire customer-trust system.

03 Why Intel Went from Its Peak into Difficulty

Intel’s problems did not emerge overnight. They represent a classic case of “the backlash of a successful path.” Intel won the PC era through the IDM model (Integrated Device Manufacturer—a vertically integrated manufacturing model in which a semiconductor company independently handles the entire value chain from chip design, manufacturing, packaging and testing to sales). But when the industry entered the mobile internet and AI eras, the original strengths began to become burdens.

1. Success in the PC era caused Intel to miss the mobile era

At Intel’s most glorious moment, its core market was PC and server CPUs. But in the mobile-internet era, smartphones and tablets rose rapidly. Apple, ARM, Qualcomm, and TSMC jointly advanced a supply chain centered on low-power, highly integrated chips.

Apple ultimately chose to develop Apple Silicon in-house because it needed higher energy efficiency and stronger hardware-software integration, rather than continued reliance on Intel’s general-purpose CPU roadmap. Apple’s shift from Intel processors to Apple Silicon was not merely a supplier substitution, but a redefinition of the idea that “chips must serve the overall device experience.”

The M1 chip was the first-generation system-on-a-chip in the Apple Silicon family; Source: AppleInsider.

2. Manufacturing delays weakened Intel’s technological halo

Intel’s core belief used to be: my process technology will always lead. But Intel later experienced repeated delays at nodes such as 10nm and 7nm, causing the market to question its manufacturing execution. Meanwhile, TSMC continued pushing 7nm, 5nm, and 3nm into volume production and gradually became the de facto global leader in advanced processes.

For Intel, this was a double blow: on the one hand, its CPU products came under pressure from competitors such as AMD; on the other hand, its once-proud manufacturing advantage was caught and even surpassed by TSMC.

3. The IDM model became increasingly heavy in the new era

The advantage of the IDM model is that design and manufacturing are integrated, giving it high coordination efficiency. The disadvantage is extremely heavy capital expenditure. Advanced-process fabs require investments that can easily run into tens of billions of dollars. If capacity mainly serves in-house products, then once growth in a company’s own CPUs slows, fab utilization comes under pressure.

TSMC is different. It serves the world’s strongest chip-design companies and can aggregate demand from Apple, Nvidia, AMD, Qualcomm, Broadcom, and others, using higher utilization rates to spread R&D and capital expenditures.

That is why Intel later found itself in an awkward situation: it had manufacturing capability, but lacked sufficiently strong external customers to support investment in advanced processes.

This is also why Apple’s orders matter so much to Intel. Apple is not an ordinary customer; it is one of the world’s most influential chip customers.

04 Why Intel Is Re-Entering Apple’s Field of Vision Now

Apple is not turning back to Intel out of nostalgia. What is driving this cooperation is the alignment of interests among three parties: Apple needs a second supply chain, Intel needs a benchmark customer, and the U.S. government needs domestic advanced manufacturing.

1. Apple needs to relieve pressure on TSMC capacity

The AI era has completely changed the supply-demand dynamics of advanced processes. In the past, advanced processes mainly served smartphones, PCs, and server CPUs. Now, AI training chips, AI inference chips, AI servers, AI PCs, and AI smartphones are all competing for the same pool of the most advanced manufacturing resources. Broadcom recently stated that TSMC capacity is becoming a supply-chain bottleneck; although TSMC will continue to expand capacity through 2027, the 2026 supply chain is already constrained.

This is critical for Apple. Although Apple remains one of TSMC’s most important customers, the competitors it now faces are no longer just handset makers, but Nvidia, AMD, Broadcom, and the AI chips of major cloud companies.

It is not that Apple does not trust TSMC, but that it cannot allow its future to be completely constrained by TSMC’s capacity allocation.

2. Intel’s foundry strategy needs a “credit endorsement”

Intel proposed its IDM 2.0 strategy as early as 2021. The core was to reinforce manufacturing capability while building Intel Foundry Services to manufacture for external customers. Intel also announced at the time a US$20 billion investment in new fabs in Arizona. But the problem is that foundry is not something Intel can simply declare itself strong in.

What customers care about is:

- whether the process is stable

- whether yield meets the standard

- whether delivery can be made on time

- whether Intel is truly willing to serve external customers

- whether it can protect customers’ design confidentiality

- whether it has a sufficiently mature EDA and IP ecosystem

In March 2025, Intel appointed Lip-Bu Tan as CEO. Tan is a veteran of the semiconductor industry, a former CEO of Cadence, and has long been deeply involved in EDA, chip design, and semiconductor investment. After he took office, what the market focused on was not a slogan, but whether Intel was truly beginning to shift from an “engineer-driven closed giant” to a “customer-driven open foundry platform.”

If Apple truly enters Intel’s foundry system, the significance for Intel will go far beyond a single order. It would be tantamount to telling the market:

Even Apple is willing to test Intel’s advanced processes, which means Intel’s foundry business is no longer just a PowerPoint story.

That would be an extremely powerful industry endorsement for Intel Foundry.

U.S. Commerce Secretary Howard Lutnick and Intel CEO Lip-Bu Tan reached a US$8.9 billion U.S. government investment agreement in August 2025; Source: KOIN.

3. The Trump administration and “Made in America” are important forces behind this deal

According to Reuters, the U.S. government played an important role in promoting the negotiations between Apple and Intel, and the agreement is also in line with the Trump administration’s goal of expanding domestic chip-manufacturing capacity in the United States. The U.S. government had previously obtained approximately a 10% stake in Intel by converting part of the CHIPS Act-related funding into equity.

This means Intel is no longer just a company. From the perspective of U.S. strategy, Intel increasingly resembles a “national semiconductor asset.”

The logic of the U.S. government is clear:

- AI is at the core of future national competition;

- advanced chips are the infrastructure of AI;

- advanced chip manufacturing cannot remain highly dependent on Asia over the long term;

- the United States must rebuild domestic advanced-process capability;

- Intel is the domestic company most likely to undertake that mission.

So Apple’s cooperation with Intel appears on the surface to be a commercial order, but at a deeper level it is also a response by the U.S. technology supply chain to the themes of domestic manufacturing, supply-chain security, and America First.

Apple will of course not sacrifice product competitiveness for politics. But if Intel’s technology roadmap is close to becoming usable, and the U.S. government is simultaneously providing policy, capital, and strategic support, then assigning Intel a portion of lower-end M-series or non-flagship chip orders would be an entirely reasonable choice.

The core of Apple’s cooperation with Intel is not that Apple intends to leave TSMC, but that Apple has realized: in the AI era, advanced-process capacity itself has become a strategic asset. Whoever controls a second supply chain will have greater initiative in the chip wars of the next decade.

In 2024, Fupeng International has successfully completed five SPAC listings, setting an annual record for a single institution in the industry.

Enterprises with clear listing plans can contact Fupeng International for negotiation. With our cutting-edge capital structure design capabilities, we help innovative enterprises seize the historic opportunities in the SPAC 2.0 era.