In July 2025, a seemingly low-profile M&A announcement drew widespread attention across both the U.S. SPAC market and the crypto community: Reeve Collins, co-founder of Tether (USDT), completed the acquisition of SPAC M3-Brigade Acquisition V Corp., officially renaming it CCRC Digital Assets Corp., and entered into a $1.5 billion Business Combination Agreement (BCA) with his newly launched venture, ReserveOne.

This was not merely a capital maneuver, but also a signal of compliance, structural innovation, and the public securitization of digital assets.

01 Reeve Collins: From Stablecoin Pioneer to Driver of Crypto Asset “Securitization”

As a co-founder of the leading stablecoin USDT, Reeve Collins has long been active in blockchain payments and Web3 infrastructure development. Unlike many crypto entrepreneurs, Collins has in recent years shifted his focus toward institutional integration of digital assets and the creation of structured financial products.

His latest project, ReserveOne, positions itself as an innovative “digital asset treasury platform anchored by mainstream cryptocurrencies such as Bitcoin and Ethereum, serving both institutional investors and retail participants.”

Chart: SPAC IPO data comparison. As of mid-2025, the number of SPAC IPOs has already surpassed the full-year total for 2024.

Unlike MicroStrategy and other “Bitcoin allocation–driven public companies,” ReserveOne enables investors to indirectly hold BTC, ETH, and stablecoins through its stock issuance. Rather than relying on operating income, its model is built around a balance-sheet–driven, crypto-denominated structure.

02 What Exactly Is ReserveOne?

Core Positioning: Turning “holding Bitcoin” into a publicly tradable security.

ReserveOne’s vision is to become a “publicly traded, institutionally regulated digital asset platform backed by Bitcoin and other cryptocurrencies.”

-

Balance sheet structure: Primarily holding BTC, ETH, and stablecoins such as USDT and USDC.

-

SPAC merger listing: Investors gain indirect exposure to these assets through holding its stock.

-

Comparison to MicroStrategy: While similar in “public listing with crypto holdings,” ReserveOne is closer to an ETF-like platform with a more institutionalized and transparent governance model.

-

Revenue model: Not reliant on traditional operating income, but rather on digital asset appreciation, structured product design, and allocation efficiency.

Pictured: ReserveOne’s official website disclosure of the types of cryptocurrencies it will hold.

Leadership Team – a Crypto-Finance “Dream Team”:

-

Reeve Collins (Executive Chairman): Tether co-founder, expert in structured crypto products.

-

Jaime Leverton (CEO): Former Hut 8 CEO, seasoned operator of a listed Bitcoin company.

-

Sebastian Bea (President): Former Coinbase Asset Management executive, with strong institutional investor experience.

-

Advisors/Directors: Former U.S. Commerce Secretary Wilbur Ross; ex-Blackstone executive Chinh Chu; Coinbase Institutional strategist John D’Agostino; Binance board member Gabriel Abed, among others.

Core Logic: Wrapping Bitcoin into a security product for institutions, family offices, and HNWIs — providing a compliant crypto allocation tool with liquidity, regulatory oversight, and composability. The ambition: to become the “Blackstone of digital assets.”

03 SPAC Transaction Path & PIPE Financing

Collins acquired control of M3-Brigade through a $6.467 million purchase of Sponsor shares and private warrants, renaming it CCRC Digital Assets, and quickly executed the BCA with ReserveOne.

The strategic centerpiece is a $750 million PIPE financing, structured as:

- $500 million: Common stock + warrants

- $250 million: Convertible notes

PIPE investor roster highlights ReserveOne’s deep industry backing and ecosystem synergies:

Infrastructure: Blockchain.com, Kraken, FalconX, Origin Protocol

Asset Management & VC: Galaxy Digital, Pantera, ParaFi, Republic Digital

Tech & Layer 2: Mantle Network, Hivemind

Traditional PE: CC Capital, Monarq Investment Partners

This represents not only capital infusion, but also ecosystem leverage in custody, liquidity, and technology.

04 Why Can Reeve Collins Be Both SPAC CEO and Target Company Chairman?

In most traditional SPAC transactions, the management of the SPAC and the target company are expected to remain at arm’s length to avoid conflicts of interest. Yet in this case, Collins is both CEO of CCRC Digital Assets (SPAC) and Executive Chairman of ReserveOne (target) — drawing market attention.

Why is this arrangement feasible in a crypto SPAC?

-

Formal conflict ≠ substantive issue: Market process is key

-

Collins acquired all Sponsor shares and warrants of the SPAC in a market transaction (≈$6.46M) from the original Sponsor, rather than setting up a SPAC from the start to acquire his own company. This bypasses strict U.S. corporate law restrictions on self-dealing SPACs.

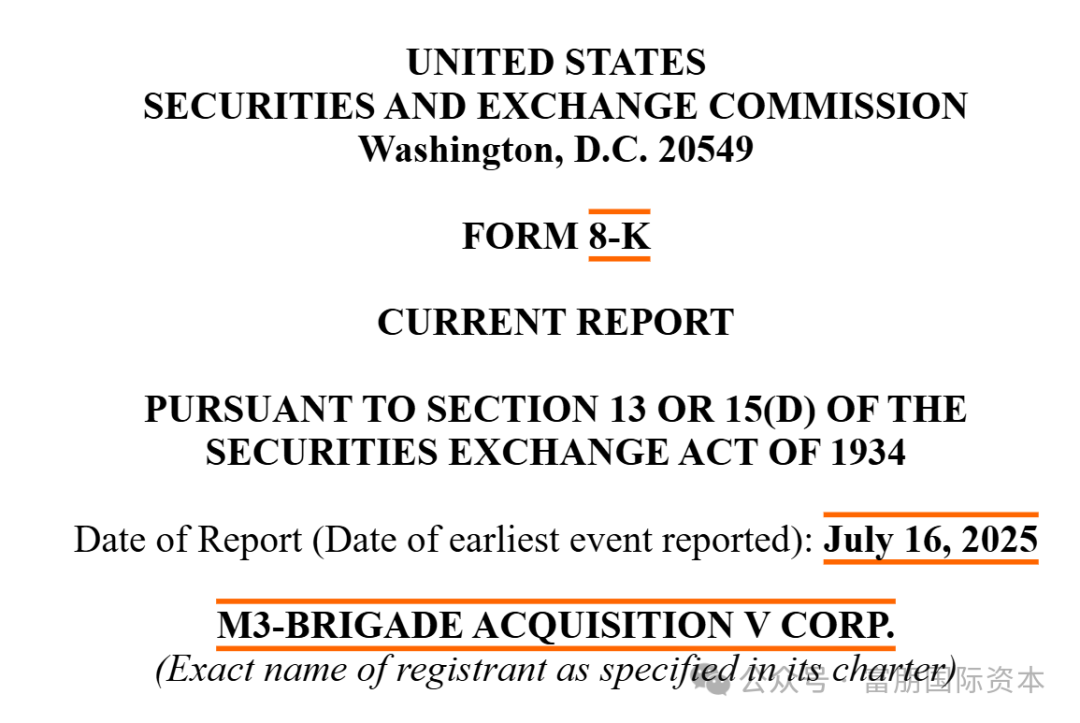

Pictured: Latest Form 8-K filing of the SPAC where Collins serves as CEO; https://www.sec.gov/ix?doc=/Archives/edgar/data/2016072/000121390025065730/ea0249460-8k_m3brigade5.htm

Pictured: Latest Form 8-K filing of the SPAC where Collins serves as CEO; https://www.sec.gov/ix?doc=/Archives/edgar/data/2016072/000121390025065730/ea0249460-8k_m3brigade5.htm -

Moreover, he did not bypass regulatory procedures but fully complied with SEC disclosure requirements by filing a Form 8-K, thereby ensuring that all investors are fully informed of his dual roles. In both the Form 8-K and the Proxy Statement, he is required to make mandatory disclosures, including:

-

Whether the SPAC management team serves as directors, executives, or indirect controllers of the target company;

-

Their equity holdings in the target company or any future equity incentive arrangements;

-

Whether they played a leading role in negotiations, valuation, or transaction terms, and whether there exists an opportunity or motive to control the deal pricing;

-

Whether they might prioritize the interests of the target company or themselves over those of public shareholders;

-

Whether they receive any additional compensation or benefits (such as target company shares, equity incentives, etc.);

-

The extent of their influence over valuation, deal terms, or timing of the transaction;

-

All interests Collins or his controlled entities obtain before or after the merger, including cash, shares, incentives, loans, management fees, and advisory fees;

-

Whether they hold advisory roles or receive service compensation from either the target company or the SPAC;

-

Whether there are any related-party arrangements in connection with PIPE investments (e.g., discounted allocations to affiliates or preferential placements).

-

-

2. PIPE Investors as a “Vote of Confidence”: Market Recognition Is the Best Proof

More importantly, ReserveOne was able to attract over $750 million in PIPE financing, with an investor roster including leading crypto institutions such as Galaxy Digital, Pantera, Kraken, and Blockchain.com. This demonstrates that these professional investors were not only fully aware of Collins’ dual role, but also chose to trust his vision and execution. In a sense, this reflects growing market acceptance of structures in which the same individual leads both the SPAC and the target company—particularly in the still not fully mainstreamed asset class of digital assets.

04 Why Do Crypto Assets Need to Go Public?

Before 2021, the crypto community largely emphasized decentralization and trustless governance systems. However, after repeated boom-and-bust cycles and heightened regulatory scrutiny, more crypto companies are now seeking legitimacy and mainstream capital endorsement, aiming to bridge into the traditional financial system.

-

Obtain regulatory status – Through SEC filings, quarterly reporting, and audit procedures, companies build market trust.

-

Access capital markets – Institutional investors often require the compliance framework of a listed company.

-

Enhance liquidity and valuation benchmarks – When crypto assets are securitized into publicly traded equity, they achieve greater liquidity and more rational valuation anchoring.

-

Secure institutional partnerships – Whether for custody, clearing, or market-making, listed status often serves as the entry ticket.

Against this backdrop, a wave of companies led by ReserveOne are leveraging SPACs to rapidly achieve compliance and securitization. This process is expected to further fuel the surge of SPAC De-SPAC listings in the U.S. market.

In 2024, Fupeng International has successfully completed five SPAC listings, setting an annual record for a single institution in the industry.

Enterprises with clear listing plans can contact Fupeng International for negotiation. With our cutting-edge capital structure design capabilities, we help innovative enterprises seize the historic opportunities in the SPAC 2.0 era.