In the first half of 2025, the SPAC market has shown a significant recovery trend. Multiple key indicators demonstrate that whether in terms of SPAC IPO volume, total deal value, or M&A activity, the market has surpassed 2023 and 2024 levels, gradually returning to a new equilibrium after the 2021 boom.

01 SPAC IPO Numbers and Fundraising Scale Surge

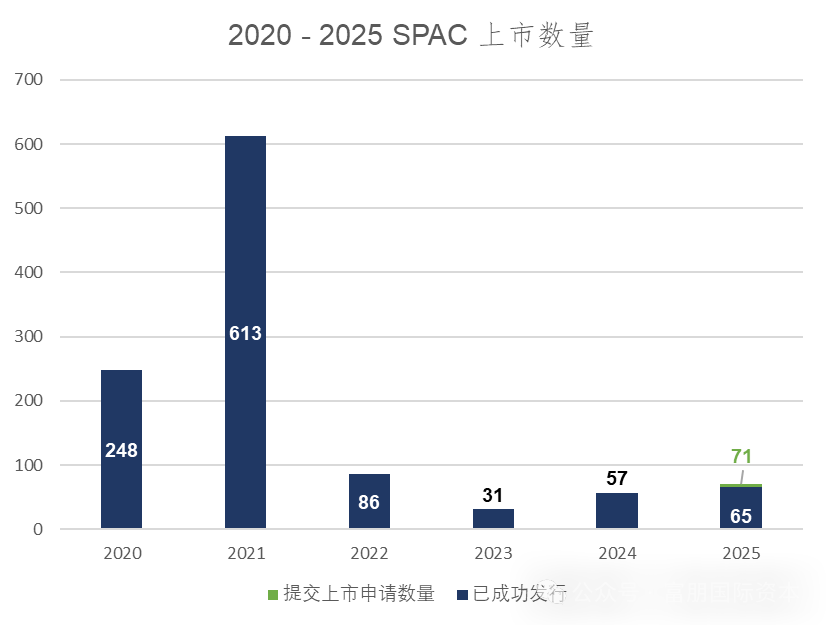

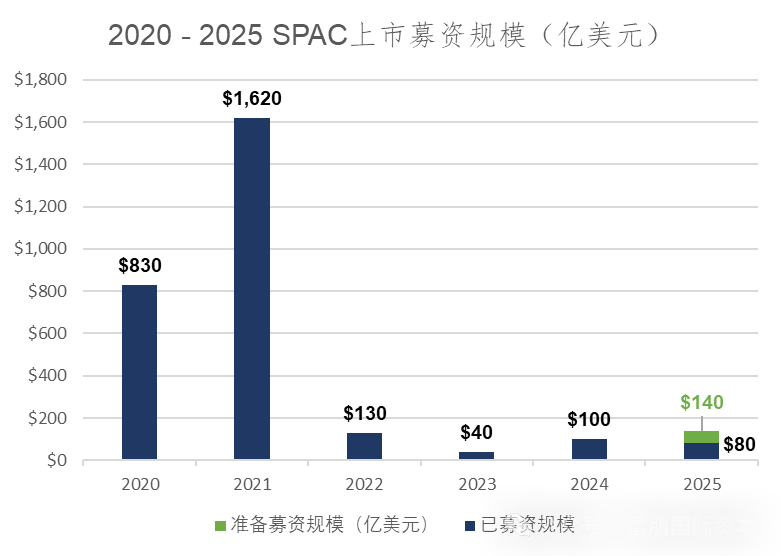

So far in 2025, 71 SPACs (Special Purpose Acquisition Companies) have filed for IPOs, of which 65 have already completed offerings, raising a total of $14 billion. This indicates a strong rebound in investor confidence toward SPACs. For comparison, SPAC fundraising totaled only $4 billion in 2023 and $10 billion in 2024 — the sharp increase highlights how SPACs are regaining recognition as effective financing vehicles.

Chart: SPAC IPO data comparison. As of mid-2025, the number of SPAC IPOs has already surpassed the full-year total for 2024.

By mid-2025, 71 SPAC filings already exceeded the 57 IPOs of 2024 in just six months. This increase reflects the optimism of SPAC sponsors about the U.S. capital markets, where more companies are expected to go public — such as cryptocurrency firms seeking listing credibility, biopharma companies requiring clinical trial funding, and oil & gas or mining companies, which were among the earliest and most frequent users of the SPAC model. The same logic is reflected in fundraising scale.

Chart: SPAC fundraising comparison. As of mid-2025, total funds raised by SPAC IPOs have already exceeded 2024’s full-year amount.

So far, SPACs have raised over $8 billion in capital already sitting in trust accounts. Including IPOs already filed, the total 2025 fundraising has reached $14 billion.

At the same time, 89 SPAC merger transactions are currently underway, representing a total deal value of $53 billion. Combined with completed transactions, the total deal value has reached $67 billion, far surpassing 2024’s $38 billion. This trend illustrates SPACs’ capital markets logic of using “small” initial funds to leverage “large” transactions, while also showing that target companies are increasingly open to SPAC mergers as a viable path to liquidity and public listing.

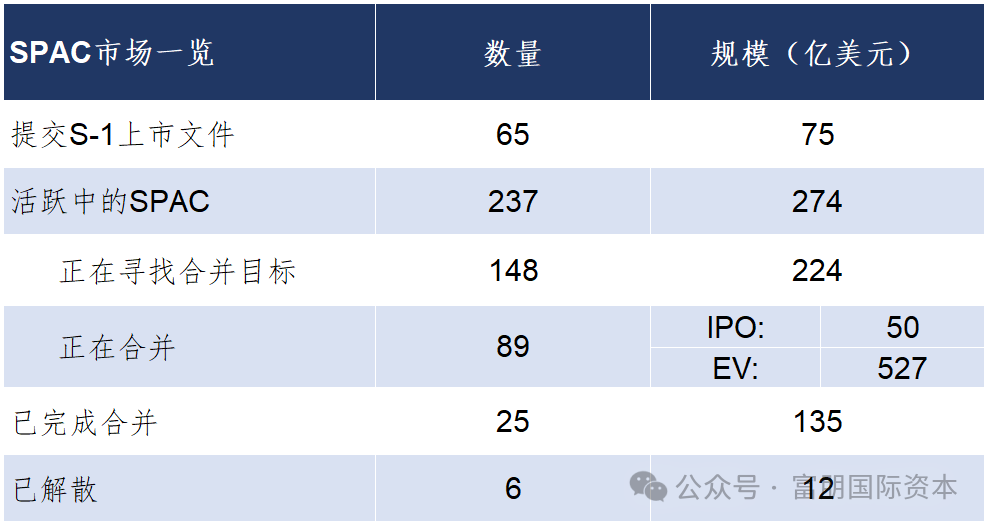

02 SPAC Ecosystem Becoming More Diverse, With 237 Active Deals

Chart: 2025 SPAC activity breakdown. Most SPACs remain in the “searching for targets” stage.

The report shows there are currently 237 active SPACs, including:

-

148 still searching for targets

-

89 in active M&A negotiations

Together, they represent a combined market value of $27.4 billion. This “deal preparation pool” suggests that the next 12 months will likely see another wave of SPAC transaction activity.

A key reason why more companies are choosing SPAC mergers is that unlike traditional IPOs, SPAC listings do not require minimum revenue or market capitalization thresholds. Moreover, the valuation and timing of going public can be more actively negotiated between the target company and the SPAC — avoiding the risk of undervaluation where much of the IPO proceeds benefit Wall Street banks instead of the company itself.

Additionally, many market participants agree that under President Donald Trump’s administration, the policy environment for SPAC listings is expected to be more stable than for traditional IPOs. Trump’s own media company, DJT (Trump Media & Technology Group), went public via a SPAC merger. His Commerce Secretary, Howard Lutnick, previously served as CEO of Cantor Fitzgerald, one of Wall Street’s most active SPAC investment banks.

Photo: U.S. President Donald Trump (left) and U.S. Commerce Secretary Howard Lutnick (right).

03 Average Valuations of Completed Deals Continue to Rise

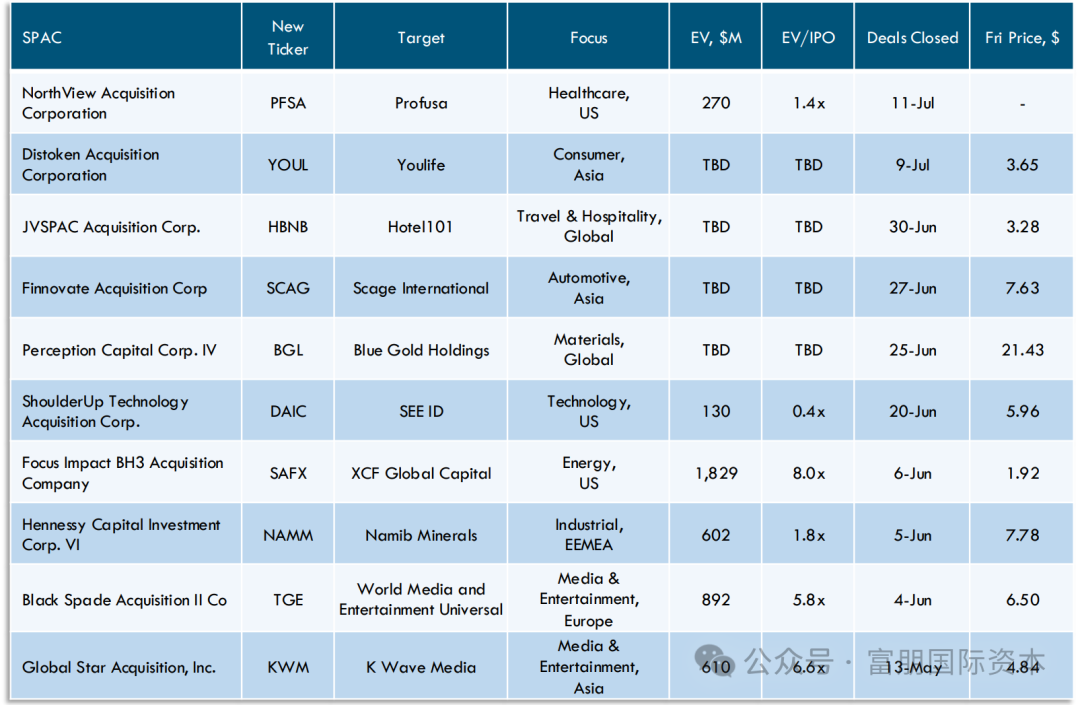

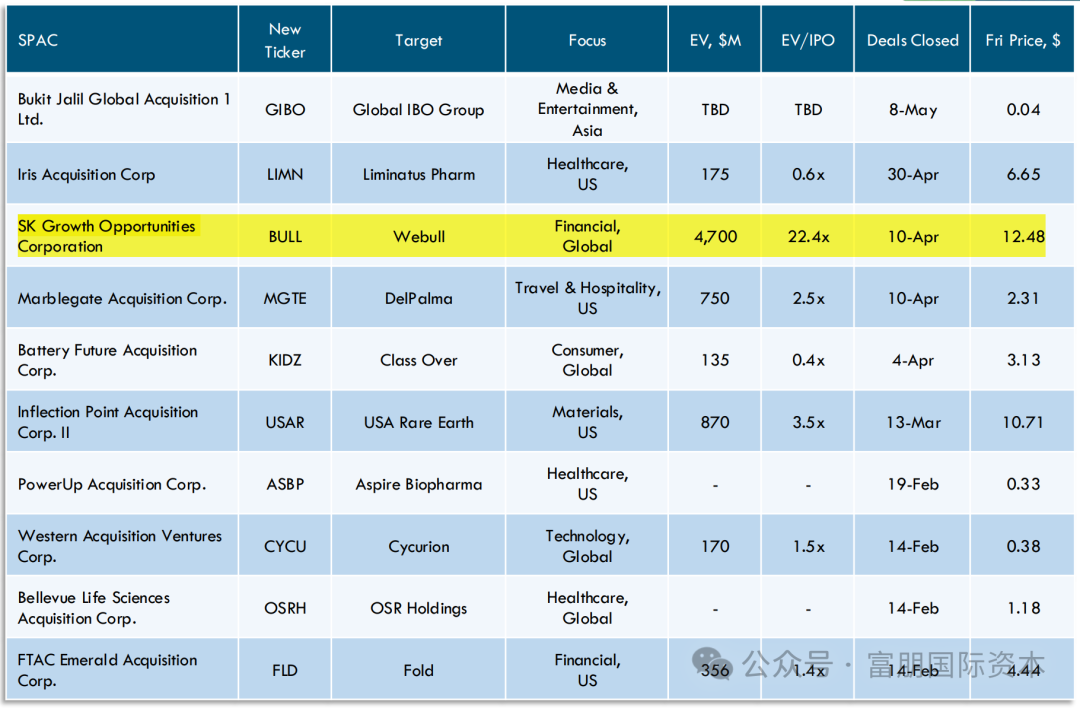

According to disclosed data, valuations of completed SPAC mergers in 2025 have significantly increased. For example, the Webull transaction was valued at $4.7 billion, with a 22.4x multiple. This demonstrates that high-growth and high-tech companies are increasingly embracing the SPAC structure, and that investors are focusing more on core enterprise value rather than short-term market fluctuations.

Chart: Selected 2025 De-SPAC (reverse merger) cases, sourced from SPAC Research.

04 Conclusion

Overall, the 2025 SPAC rebound is not a short-lived phenomenon. Instead, it is built on a more mature regulatory framework, optimized deal structures, and greater investor awareness. For companies planning a U.S. listing, SPACs are emerging as a more controllable and flexible window of opportunity.

Chart: “Two-way choice” — Our expertise makes us the partner worth your choice.

In 2024, Fupeng International has successfully completed five SPAC listings, setting an annual record for a single institution in the industry.

Enterprises with clear listing plans can contact Fupeng International for negotiation. With our cutting-edge capital structure design capabilities, we help innovative enterprises seize the historic opportunities in the SPAC 2.0 era.