01 What is a SPAC?

SPAC is the abbreviation of Special Purpose Acquisition Company in English, which is translated into Chinese as “Special Purpose Acquisition Company”.

SPAC is a company established by SPAC sponsors for the purpose of acquiring (merging) other operating companies. It is actually a shell company. It does not and will not conduct any actual business. It is a legal vehicle and a financial instrument for raising funds to acquire other companies. After its establishment, SPAC can first legally raise funds in the capital market and become a listed company at the same time, and then acquire (merge) a private company with actual operating business (referred to as the target company) by issuing additional shares, that is, through SPAC merger (merger) transactions or “De-SPAC Transactions”, the target company of the merger (merger) becomes a listed company. The SPAC model allows the target company to become a listed company and obtain more funds to promote corporate development, while also obtaining returns for SPAC sponsors, SPAC investors and target company shareholders.

02 The History of SPACs

The first stage can be called the “emergence period”

SPAC was introduced to the U.S. capital market by GNK Securities in 1993. It uses shell companies with no business to raise funds in the open market, and then uses the raised funds to reverse merge high-quality target companies to help the target companies achieve the purpose of listing and financing. It was also in this year that “SPAC” became a globally recognized name.

从1990年到1994年,资本市场一共完成了15家通过SPAC合并完成上市;此后从1995年到2002年约7年时间中,SPAC合并交易活动一度停滞。

The second stage is the “growth stage” of SPAC

From 2003 to 2008, there were 161 SPACs listed, and the total amount of SPAC funds raised reached US$21.9 billion, which was mainly due to the rapid development of private equity funds (PE). After the outbreak of the financial crisis in 2008, SPAC-related activities once dropped to a freezing point. In 2009, the first year after the financial storm, only one SPAC in the US capital market achieved an IPO. After 2010, when the US financial market gradually emerged from the shadow of the subprime mortgage crisis, the SPAC model was once again warmly welcomed by secondary market investors. In the eight years from 2010 to 2018, a total of 167 SPACs were listed in the US capital market, and the amount of SPAC funds raised reached US$33.5 billion.

图为查马斯 Source: New York Times

The third stage is the “explosion period” of SPAC

According to SPAC Analytics data, in 2019, there were 59 SPACs listed, accounting for 28% of all IPOs, and the amount of SPAC financing was US$13.6 billion, accounting for 19% of the total funds raised by all listings. By 2020, SPAC listings surpassed traditional IPOs for the first time, reaching 248, accounting for 55% of all IPOs, and the amount of SPAC financing reached US$83.4 billion, accounting for 46% of the total funds raised by all listings. By 2021, there were 613 SPACs listed in the United States, accounting for 63% of the number of IPOs, and the amount of SPAC financing had reached more than 160 billion, nearly twice that of 2020, accounting for 49% of the total funds raised by all listings.Since 2019, the explosive growth of SPAC listings in the United States has attracted the attention of global capital and markets, and Chamath is one of the protagonists in this capital fairy tale.

03 SPAC KING

The picture shows Chamath announcing that his SPAC “IPOA” will merge with Virgin Galactic Source: Bloomberg

After IPOA was established, it entered a long waiting period. During this period, the founder had to look for targets and negotiate acquisitions. The stock price was also firmly set at 10 yuan and hardly moved. Because SPAC did not have any physical operating activities, the stock price perfectly reflected the value of the cash in the trust account.

In July 2019, less than three months before the agreed acquisition deadline, IPOA announced that it had found an investment target, Virgin Galactic.

According to the acquisition agreement, the acquisition price of Virgin Galactic was US$1.3 billion.

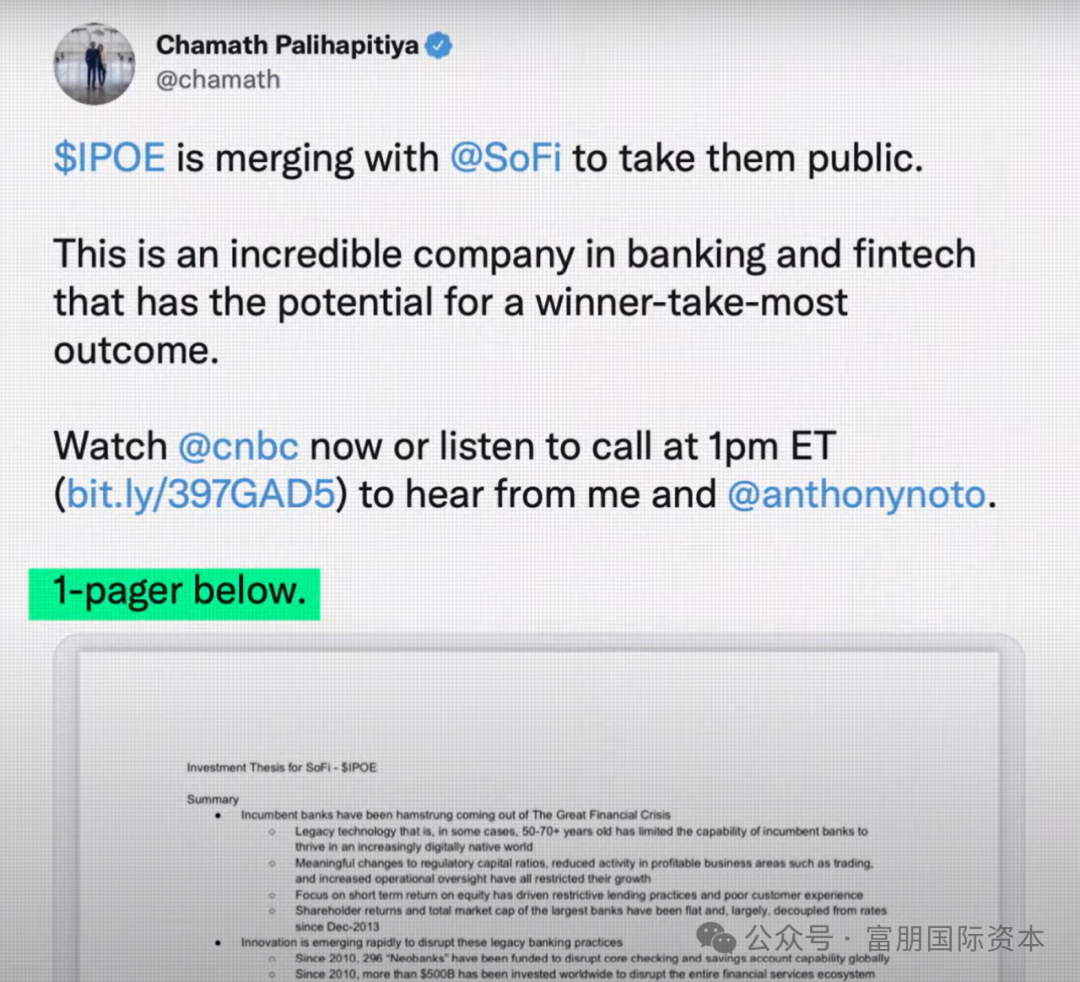

Every time SPAC finds a target company, Chamath will post on social media why he wants to merge with the target company and go public. As of May 2025, Chamath’s social media has 1.88 million followers.

With his industry influence as a successful venture capital investor, Chamath frequently shared the analysis logic and prospects of SPAC acquisition target companies through social media, successfully igniting the enthusiasm of retail investors to participate. He simplified the complex capital operation into a popular metaphor of “opening a blind box of high growth potential”, and emphasized that the SPAC model broke the information monopoly of institutional investors in traditional IPOs and gave ordinary people the right to access early star projects. This highly contagious expression, coupled with his legendary resume of early investments in giants such as Amazon and Tesla, made a large number of retail investors believe that following his SPAC layout can replicate the “profit myth” in the Virgin Galactic case. The public market SPAC shares of $10 per share were hyped up to $15 per share by retail investors, which is equivalent to using $15 to buy shares worth $10, and the hope of profit is completely pinned on Chamath to find another super growth company for listing and merger. Chamath also struck while the iron was hot and released more SPACs in alphabetical order – “IPOB”, “IPOC”, “IPOD”…

04 After the craze fades, SPAC becomes a new path to listing

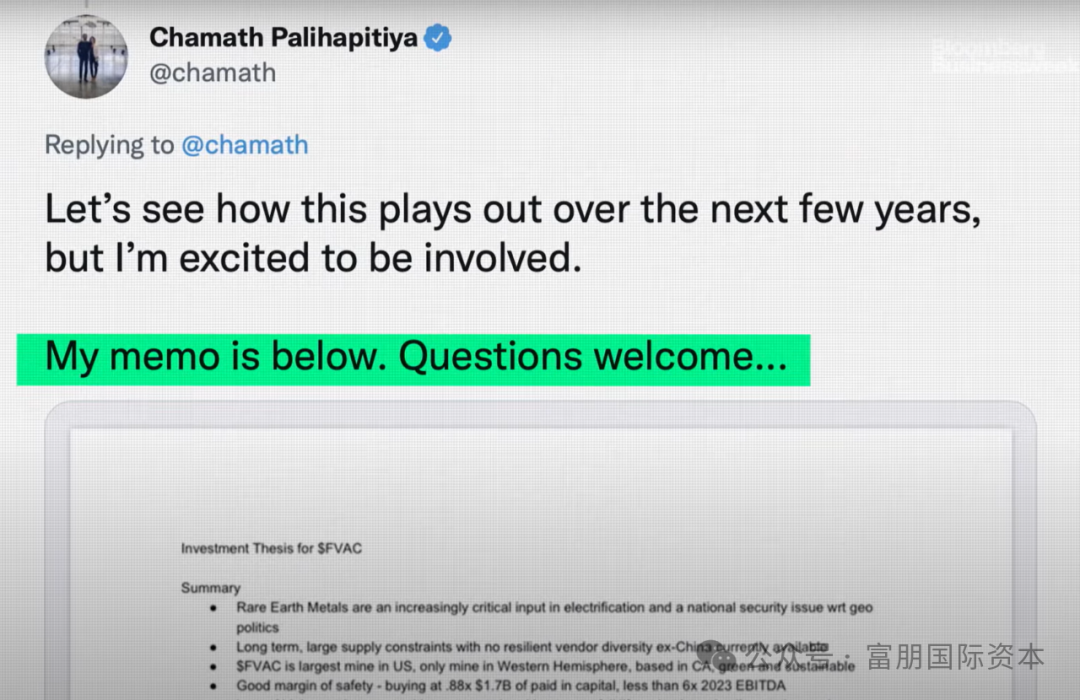

The picture shows Chamath announcing that his SPAC “IPOC” will merge with medical technology company Clover Health Source: Bloomberg

Clover Health focuses on the Medicare Advantage business and optimizes the medical cost management of the elderly through the data-driven “Clover Assistant” software. The merger was at the time of the SPAC boom, and investors had high expectations for the high growth of the medical technology track.

Hindenburg Research’s short-selling allegations

Hindenburg Research released a report in February 2021, revealing three major problems with Clover Health:

(1) It failed to disclose the U.S. Department of Justice’s investigation into its alleged kickbacks, improper marketing, and related-party transactions;

(2) The actual effects of the “Clover Assistant” software were exaggerated and faced regulatory scrutiny;

(3) The business model was unsustainable and may face “survival risks”

On the day the report was released, Clover’s stock price plummeted 15%, and in the following weeks, the cumulative decline exceeded 31%. Investors questioned whether Chamath did not conduct sufficient due diligence before the merger. When the craze subsided, Chamath closed several SPACs that had not completed mergers. As of May 2025, Clover Health is still dealing with the Department of Justice investigation, and its stock price has fallen by about 80% from its high point at the time of the merger, with its market value shrinking to about US$1.5 billion.

05 From enthusiasm to rationality, a new paradigm for corporate listing

Time cost compression: The SPAC merger cycle is on average more than 50% shorter than traditional IPO.

Financing certainty is enhanced: SPAC locks in a capital pool through the “fundraising first, then M&A” model, avoiding the risk of issuance failure caused by market fluctuations in traditional IPOs. In 2024, PIPE financing exceeded US$1.8 billion, providing stable financial support for M&A.

Flexible valuation negotiation: Target companies can negotiate valuations directly with SPAC sponsors to avoid the uncertainty of public roadshow pricing. For example, Trump’s Truth Social went public through SPAC at a valuation of US$5.5 billion, with a combined redemption rate as low as 0.14%, demonstrating its negotiation advantage.

Following the new paradigm of cross-border capital, Fupeng International is the investment bank with the most US-listed SPAC shell resources, aiming to serve more companies to go public in the United States and explore win-win opportunities for cooperation. We adopt a frank and pragmatic attitude to avoid the mistakes made by Chamas.